Evaluating Novo Nordisk

Criteria #1: I like to see consistent revenue growth over time.

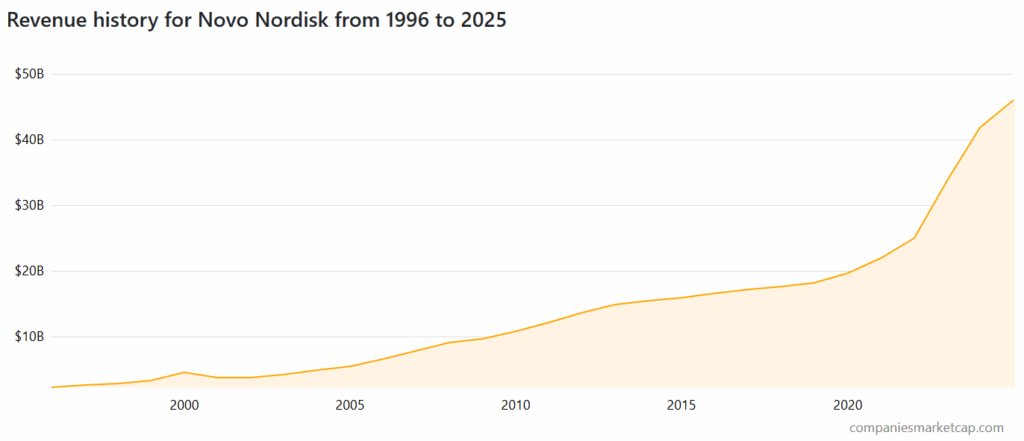

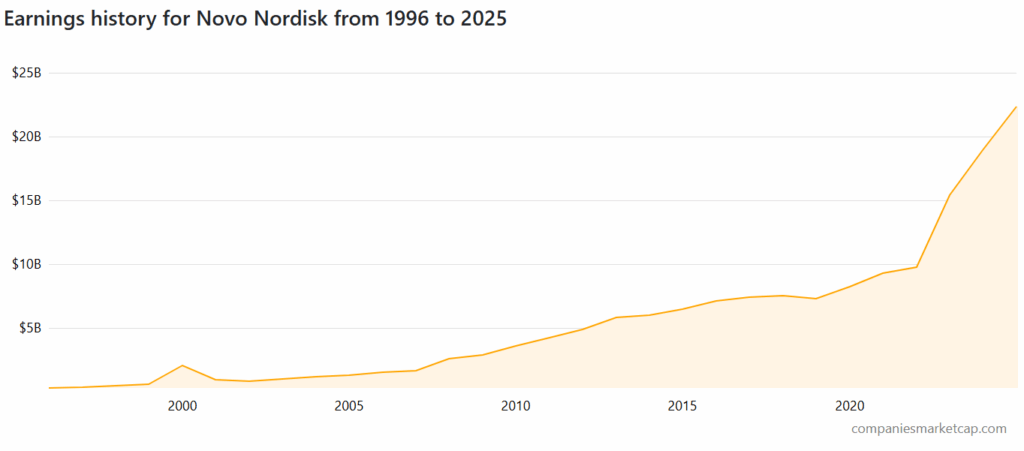

To start, let’s look at how its revenue and earnings have grown over time.

Novo Nordisk appears to grow its revenue consistently over time. Of course, it’s hit a home run with its weight loss drug, Ozempic. As I mentioned in the Eli Lilly analysis, there is an almost unlimited demand for weight loss in our current society and Ozempic is the industry leader.

The company made $20 billion in profit on $40 billion in revenue, so their margins are healthy.

Criteria #2: Is the stock reasonably priced?

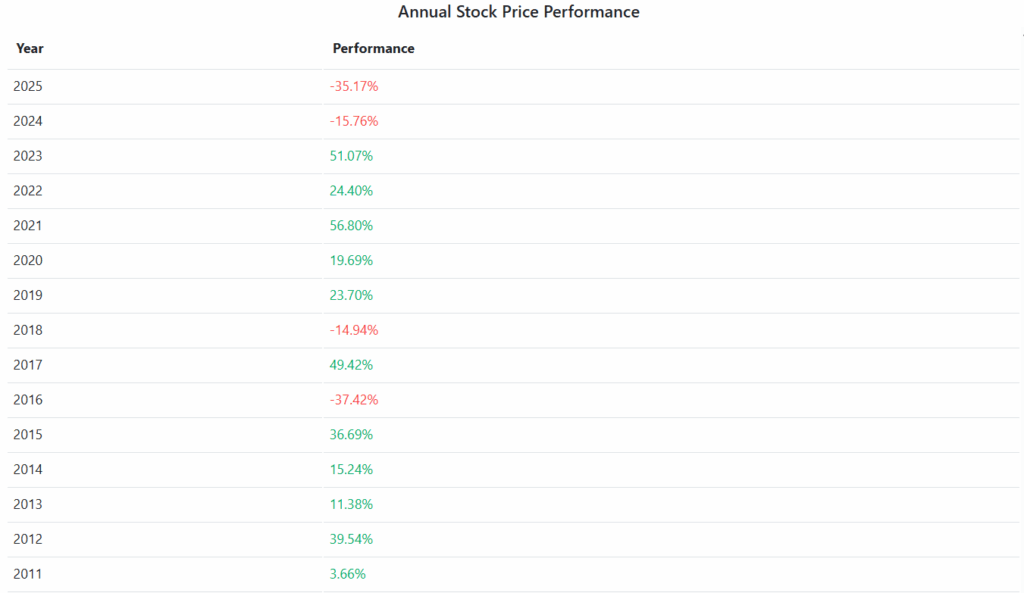

As competition intensifies in the weight loss space, the stock price has dropped significantly.

Novo Nordisk stock has fallen more than 50% in the past 12 months and is down to a reasonable P/E of 15x. That’s actually well below the market average.

One reason for this depressed price is that the patent for their star drug is expiring next year in several countries, including Canada, and generics are hitting the market. They are being forced to reduce the price of their drug from $800-$1000 per month to more reasonable levels.

Criteria #3: What is the story that will drive the company to success?

The company currently holds the leading market share for weight loss drugs. Competitors are emerging, but Ozempic is still the leader in the space.

Their future drug pipeline might not be as strong as that of larger drug companies, but this gives them room to focus on serving that one market. They are printing money – $20B profit per year – and that gives them a healthy bank account to weather future storms.

What ChatGPT Says

The Case For Novo Nordisk (Long-Term Bull Thesis)

- Attractive Valuation

- Novo Nordisk trades at a forward P/E of approximately 15.6x, which is lower than the medical sector average of around 82x, suggesting relative affordability.

- Some analysts view the stock as undervalued, pointing to continued 20%+ growth in revenue and earnings.

- Thriving GLP-1 Franchise (Ozempic & Wegovy)

- These blockbuster products dominate the obesity and diabetes market, and are key drivers of the company’s outsized revenue growth.

- Patent extensions through mechanisms like PTA/PTE extend U.S. exclusivity into 2031, with generics unlikely before 2032.

- Expanding into New Therapeutic Areas

- Novo Nordisk recently earned FDA approval to treat MASH (metabolic dysfunction-associated steatohepatitis) with Wegovy, tapping into a potential $8.4 billion market by 2033.

- Strong Cash Flow Enables M&A and Infrastructure

- Excess cash from GLP-1 revenues allows for strategic acquisitions and expanding manufacturing, securing capacity and innovation.

The Case Against Novo Nordisk (Bear Thesis)

- Patent and IP Vulnerabilities

- A lapse in Canada’s semaglutide patent (due to a missed fee) now allows generics as early as 2026, potentially undercutting pricing in that market.

- Compounded (and generic) versions of Ozempic continue to erode exclusivity, particularly in the U.S., where enforcement has struggled.

- Regulatory and Competitive Headwinds

- UBS recently downgraded NVO, citing compounded competitors and a revised lower 2025 sales growth forecast of 8–14% (down from 13–21%).

- The rising market share of Eli Lilly and the spread of cheaper alternatives pose real threats to growth.

- Margin of Safety Is Thin

- At a PEG ratio near 1.96 and P/B around 9.9, valuation may be stretched if growth slows or expectations are unmet.

- Operational and Legal Complexity

- Controversy over generic alternatives and pricing strategies (especially amid U.S. political scrutiny) adds execution risk and regulatory uncertainty.

Final Thought

Novo Nordisk currently offers defensive growth with a healthy valuation compared to peers – but it’s not without risks. If they maintain GLP-1 dominance, scale in MASH, and stave off generics, the upside remains compelling. However, any disruption in exclusivity, pricing, or expansion execution means there’s a limited buffer for investors.

Conclusion

I will buy a few shares of Novo Nordisk based on it being oversold and Ozempic being a clear leader in the space.

I bought 200 shares of Novo Nordisk (NOV.DE) for the Divchallenge Portfolio.