Evaluating Eli Lilly

I am still deciding what my first investment should be. A friend suggested Eli Lilly, so let’s see how it is.

Criteria #1: I like to see consistent revenue growth over time.

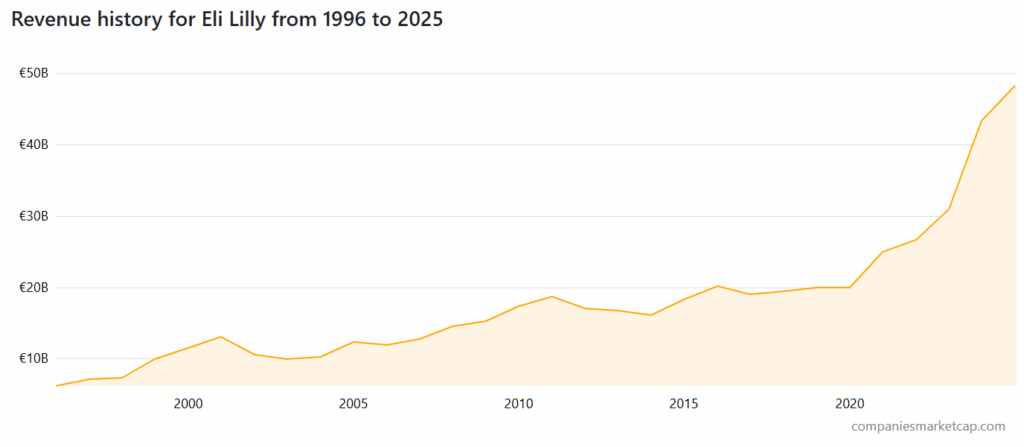

To start, let’s look at how its revenue and earnings have grown over time.

Eli Lilly appears to grow its revenue consistently over time. If it has a bad year, revenue falls by a few percent, but in a good year, revenue grows by 20-30%. The growth of the last 5 years has been higher than historical, which might not last.

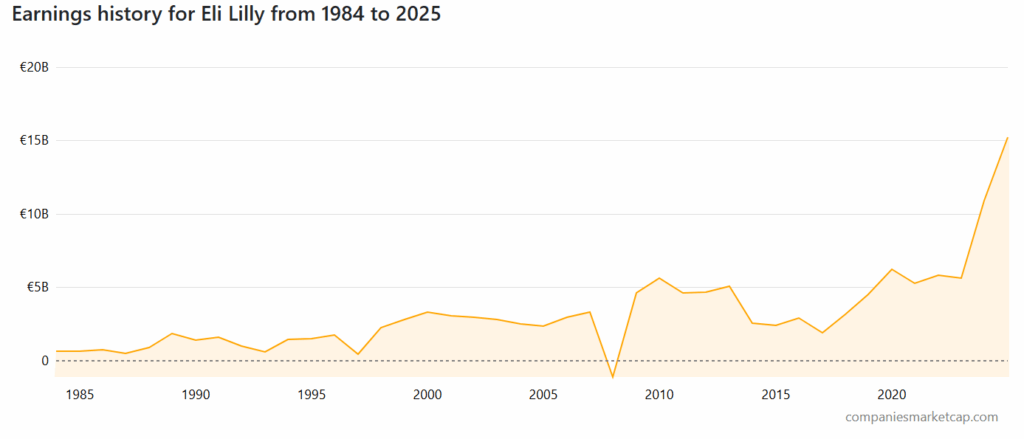

They’re profitable and they haven’t posted a loss in 15 years. Earnings growth is not consistent, but that might be the drug business overall. Margins appear to be healthy (30%+), since they have earned €10B on revenue of €43B.

Criteria #2: Is the stock reasonably priced?

There’s no point in buying a stock that already has a crazy valuation.

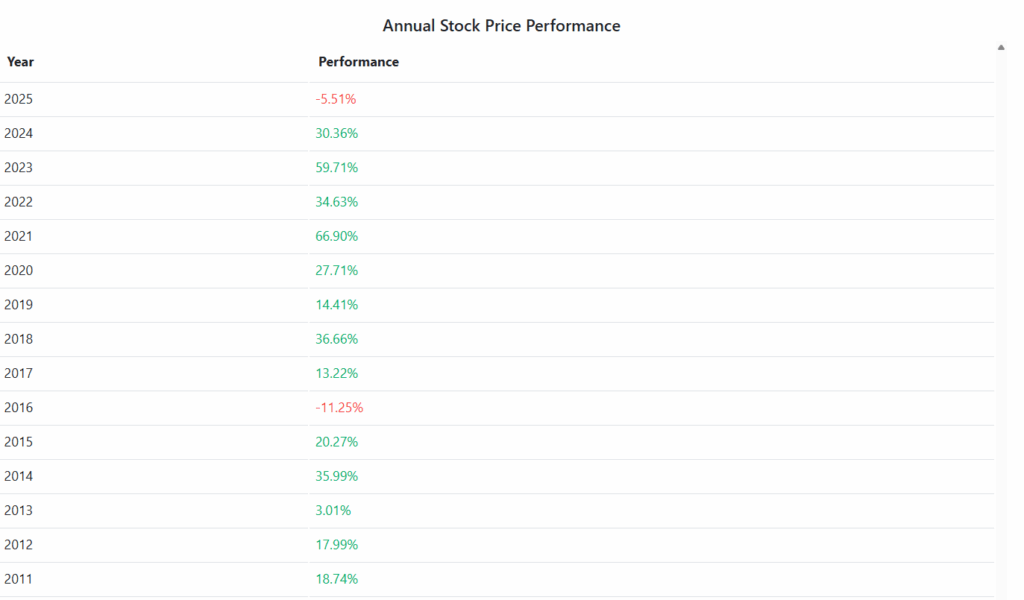

One problem could be that the stock price has skyrocketed to an extremely high level. The current P/E is 47.8, which is high outside of tech companies. But again, they have high margins and a promising drug pipeline.

The stock price growth worries me, because it’s like trying to catch a rocket ship after it’s already taken off and is starting to come back down to Earth.

I should have invested in it 10 years ago at €60 per share instead of €600 per share.

On the other hand, the stock is down 27% in 1 year. Perhaps the rocket has come down to a reasonable price.

Criteria #3: What is the story that will drive the company to success?

Eli Lilly is the maker of one of the more popular obesity drugs, Mounjaro, and as you know, the world needs weight loss drugs. And they just passed a promising trial of another weight loss drug (a pill) that helped a lot of people lose a lot of weight.

Eli Lilly uses tirzepatide for its weight loss, while Novo Nordisk uses semaglutide. They are competitors. Novo Nordisk has just announced price cuts for its Wegovy product, which could lead to price pressures.

As well, generics of semaglutide are about to hit the market in several countries. Which will lead to more price pressures.

Eli Lilly currently pays a dividend of just less than 1%.

Here’s What ChatGPT Says

✅ The Case For Eli Lilly (Long-Term Bull Thesis)

- Explosive Revenue Growth from GLP-1 Drugs

- Mounjaro (tirzepatide) for diabetes and Zepbound for obesity could generate tens of billions annually if adoption continues.

- Analysts project obesity/diabetes market size of $50B+ by 2030, with Lilly and Novo Nordisk leading.

- Pipeline Beyond GLP-1s

- Alzheimer’s drug donanemab has received FDA approval (July 2024).

- Strong late-stage pipeline in oncology, immunology, and neuroscience diversifies revenue.

- Wide Economic Moat

- Patent protection on tirzepatide into the mid-2030s gives Lilly a multi-year runway before generics.

- Strong brand trust and entrenched distribution in pharma markets.

- Earnings Catch-Up to Valuation

- Current high P/E reflects low present earnings vs. huge projected future earnings.

- If earnings scale as projected, today’s valuation could “grow into itself.”

- Defensive + Growth

- Healthcare demand is resilient in recessions, while obesity/diabetes is a secular growth trend.

- A rare “growth + defensiveness” stock, often commanding a premium.

❌ The Case Against Eli Lilly (Bear Thesis)

- Extremely High Valuation

- Forward P/E well above pharma peers (often 40–50x vs. 15–20x sector average).

- Market is already pricing in massive success — little margin of safety if growth stumbles.

- Concentration Risk in GLP-1s

- Revenue growth is heavily dependent on tirzepatide’s continued success.

- If a safety issue, competitor breakthrough, or slower uptake occurs, growth could stall.

- Patent Expiration Risk (Longer-Term)

- While tirzepatide patents run into the 2030s, eventual generic erosion is inevitable.

- Earlier expirations abroad (Canada 2026, India, etc.) could pressure international sales.

- Competition Heating Up

- Novo Nordisk remains a fierce rival with semaglutide.

- Other pharma companies (Pfizer, Amgen, AstraZeneca) are developing next-gen obesity treatments.

- Execution & Supply Chain Risks

- Lilly has struggled with supply shortages of GLP-1s due to surging demand.

- Scaling production without bottlenecks is critical — failure could limit revenue growth.

- Priced for Perfection

- At today’s valuation, Lilly must deliver flawless execution on GLP-1s and meaningful success from its broader pipeline.

- Any setback (delayed FDA approvals, trial failures, regulatory hurdles) could lead to a sharp pullback.

📌 Balanced View:

Eli Lilly is priced as if it will dominate the obesity/diabetes market and convert pipeline drugs into blockbusters. If it delivers, long-term investors could still do very well even at a high P/E today. But the risk is that the stock leaves little room for disappointment — it’s a classic “growth at a very high price” situation.

Conclusion

I want to like Eli Lilly. I want to buy it for my public portfolio. But perhaps it’s not the best first choice for a purchase.

This is on the waiting list for consideration.