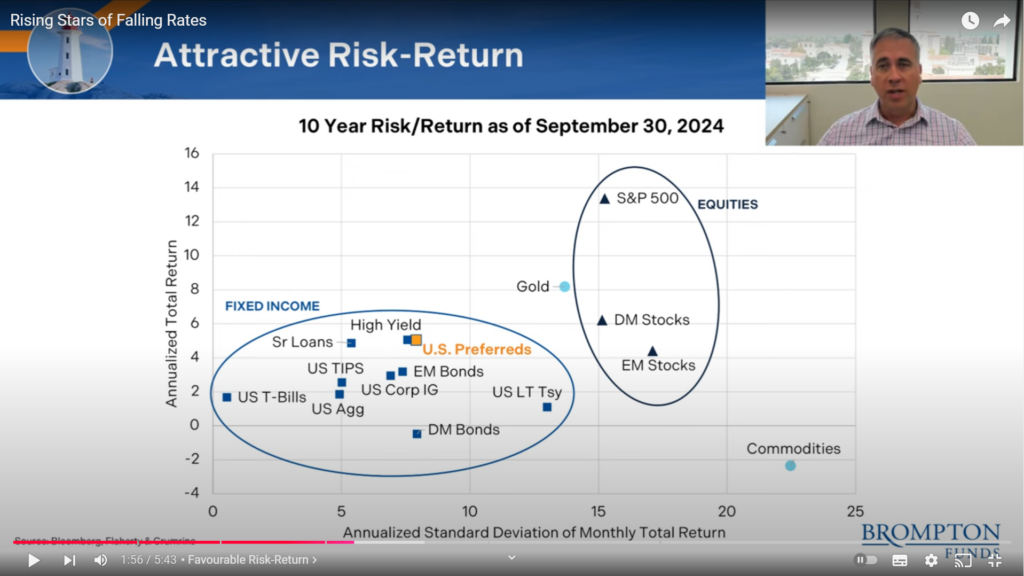

The End of Fixed Income?

I saw an interesting chart today.

The conclusion can be that investing in stocks, while riskier, averages out to a higher return in the end. And thus, it’s pointless to invest in fixed income products. If you can survive without the money invested in your account for, 10 years say, you are always better off in stocks.

My gut reaction is that 10 years is not “long term”. What about 25 or 40 years? 10 years isn’t a fair length of time to compare assets classes as we’ve been through an extended period of a stock market bull run.

But then again, 2020 has a massive crash and recovered in the same year… and 2022 had a stock market crash… and 2018 had a crash. And 2015 was a bad year for all assets. So there were some bad years in there.

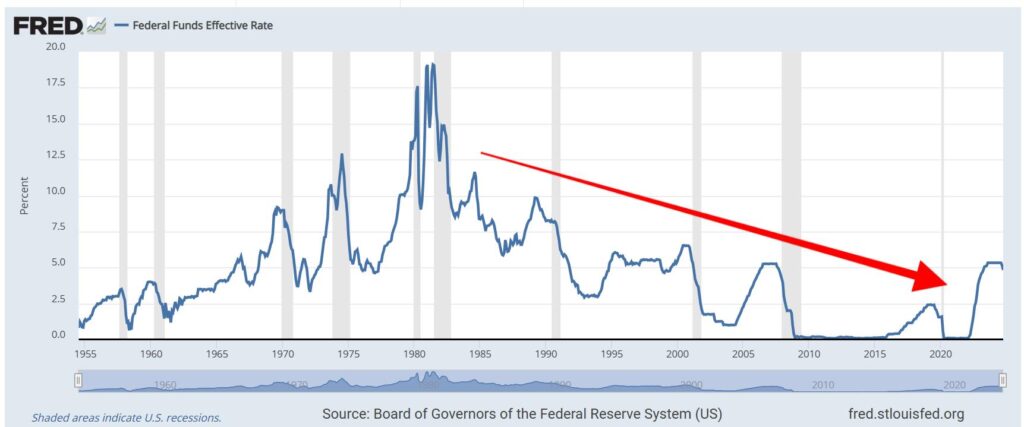

Even though 10 years is not the same as 40 years for the sake of comparison, perhaps there are some changing trends. Interest rates have been pushing towards zero, and many believe they will again. The government has too much debt to afford paying high interest rates for it. And there’s too much money in the world to hold the governments to account for their debt. Trillions of dollars in cash are chasing trillions of dollars in loans to make some type of return.

So in a low interest rate environment, does it make sense for an individual to invest in US government T-bills or US government bonds? They return 2% on average. A lousy 2%. Doesn’t make much sense! Or invest in corporate bonds like Apple or Microsoft who also pay a meager return? Or Europe who likes negative interest rates? Or Japan who likes 0%?

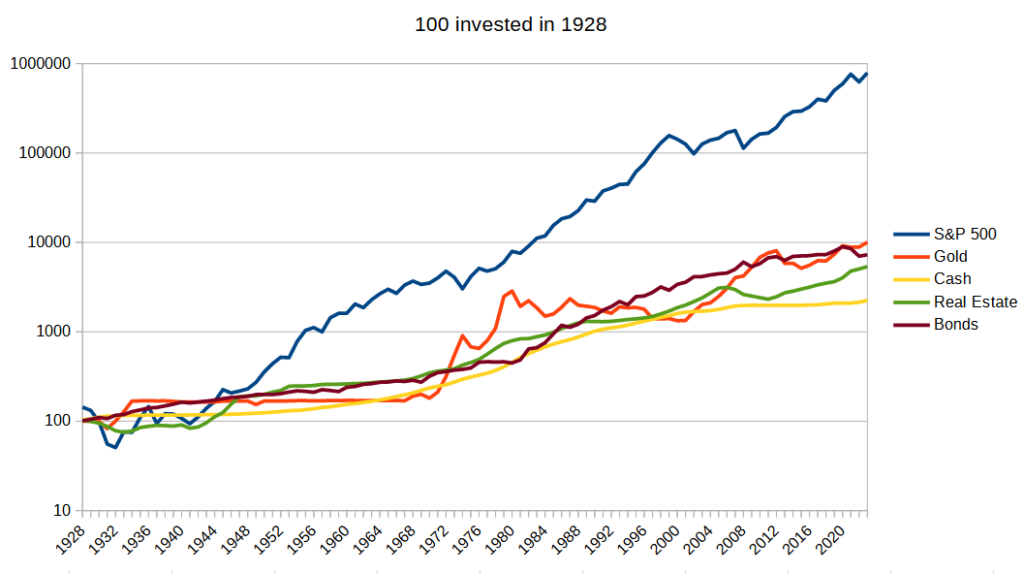

So some of that money is now chasing stocks. And we get a constant 10%-20% return in US and international stocks.

I don’t know anymore. Cash, T-bills and bonds are such awful places to return money. Even though stocks can crash for a few months, they tend to bounce back the following year. We haven’t had a multi-year decline since the 2008 global financial crisis…

Preferred shares, which I have been liking lately, are also lumped into the “fixed income is dead” pile by some. I am not so sure.

Preferred shares, if you catch them cheap, are forced to return 8-9% per year in some cases. I purchased BPO Class I and Class G preferred shares for around $11 earlier this year, and now they trade around $17. I am earning around 14% per year on my cost, while the company is only paying 9% on the money it borrowed. Even when they reset (in 2027 and 2028), the returns will only drop 1-2%.

As of today, I have:

- 11.9% in cash, uninvested (I know, I know) – 0% interest rate

- 1.3% in money market funds – 4% average dividend (ZMMK)

- 16.9% in preferred shares – 10.5% average dividend (my holdings)

- 0.4% in gold – 5.8% average distribution rate (HGY)

- 44.5% in US stocks – 34% 12 mo. return (S&P 500)

- 23.3% in International stocks – 25.6% 12 mo. return (VT)

Maybe I don’t need to hold gold. And holding money market funds is redundant given how much cash I have outside of my brokerage accounts.

I guess, in conclusion, that I remain happy with my holdings (save for those couple) and am glad I don’t hold any treasuries or government bonds. 60/40 is dead.