Time Marches On: Where to Invest Ongoing Income?

This week I have a problem that most people would not consider a problem. OK, it’s not really a problem. But it’s a unique reality.

Every month, as my clients pay me, cash is added to my business account. I don’t actually need that cash immediately to run the business. So the cash stocks up.

My goal (as outlined on this blog), is to become more fully invested in the market. So any income I get sets that goal back a bit.

How much of a problem is this?

On Wednesday, my investable net worth will increase by around 5.3%.

I currently have around 68% of my total investable net worth invested. On Wednesday, that’ll bump up to 70%.

My Money Needs a Safe Space

I should consider a rule for all the new cash that comes in. It should automatically go into some account earning interest until I’m ready to use it. There needs to be no thought required for this. Take the money, and throw it into X earning 1% interest or something.

In fact, if I can find such a safe place to store it, I can do that will all my money. I need to find a safe place to store money. Besides a 0% checking account.

This is an ongoing problem. What to do with my cash on hand? I currently have 29% of my cash in that GIC, and 37% of it parked outside…

And So…

I looked at a number of stock screeners to try to find a stock that has really low volatility (Beta). If a stock was trading at $9 five years ago, $9.50 last year, and is $10 this year, that’s a good candidate.

There’s no point in investing in such stock if there is no dividend. I might as well keep that money in the checking account if the stock never moves AND it doesn’t pay a dividend.

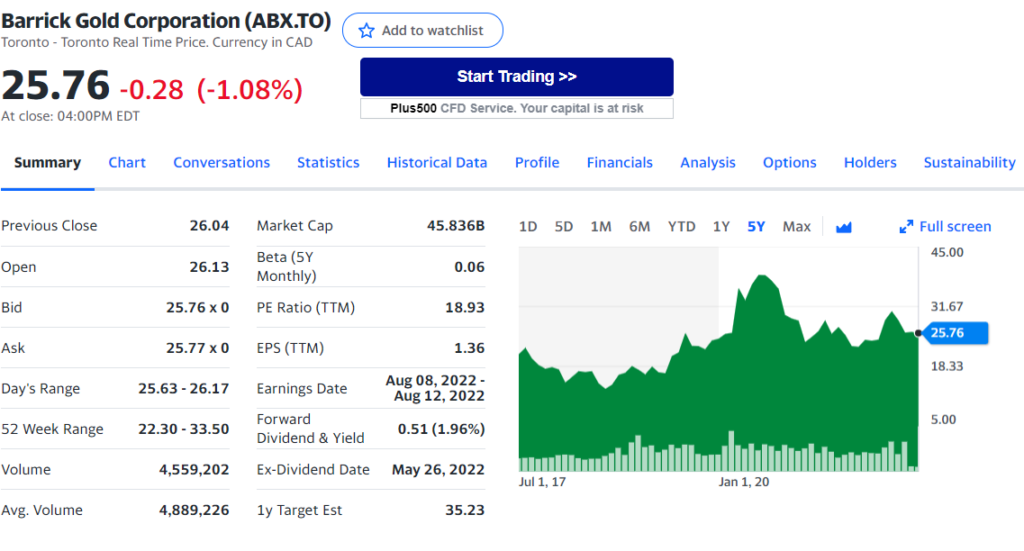

A stock like Barrick Gold (ABX) seems to fit such criteria. It was around $22 five years ago and is $26 today. It has a beta of 0.06 so it REALLY is not correlated with the stock index. And pays a dividend yield of around 2%.

That’s not too high, but there’s also the possibility of the price of gold taking off and the gold miner being a good long-term pick.

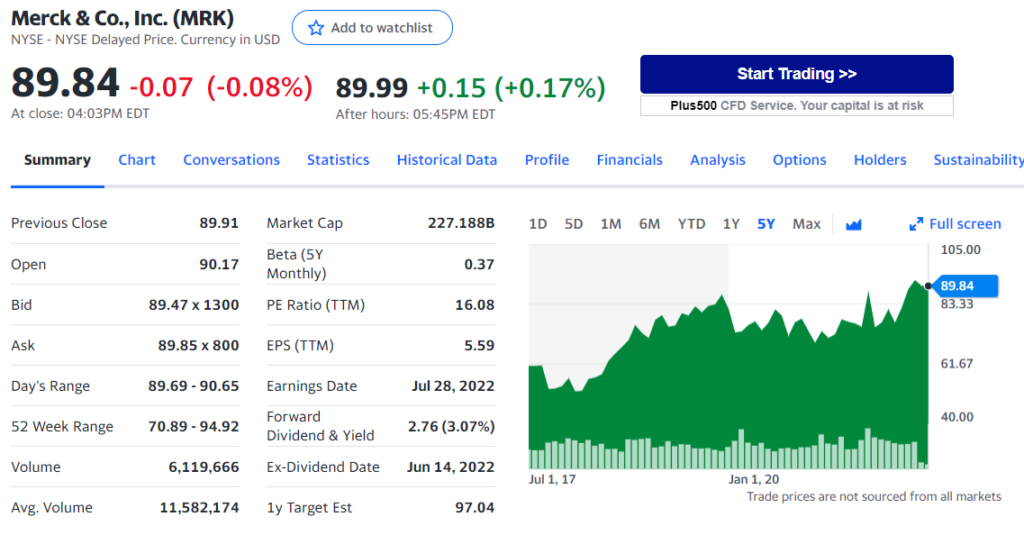

Maybe a single company is not diverse enough. Merck is also a similar company that has a beta of 0.37, fairly stable stock price over the last 5 years, and pays a 3% dividend. Better.

Maybe even better would be to find an ETF that finds such companies. High dividend and low volatility. Just reliable cash payers.

BMO has ETFs that cover this type of scenario. One is the Low Volatility Canadian Equity ETF (ZLB).

I like that 5-year price chart. Beta is not calculated, but the dips on that are not bad. This ETF is not going to crash. And the yield is 2.49% which is higher than my GIC. 🙂

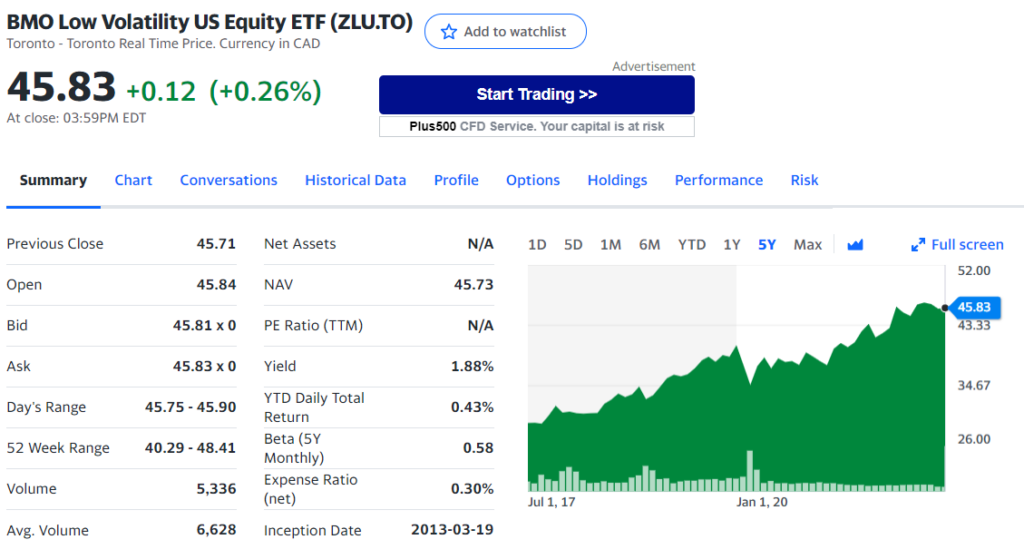

There’s also an American ETF that looks even better.

The stock is up 50% in the last five years. It’s supposed to be a low volatility ETF, but it has decent gains! And a smaller 1.88% yield. Low expense ratio. But also low average trading volume.

Looking at ZLU holdings, I like the list. Domino’s Pizza as #1 holding!

McDonald’s in there. J&J. Some good “safe” names.

Conclusion

I think I’m going to do it. The rest of my cash into ZLB and ZLU, equally.

Should I call that “fully and efficiently invested”? That’s a good question.

I’m considering this parking money while I wait for the economy to either crash or recover. But I guess technically this is invested money.

The problem is that it’s not getting me near my goal of 8% average return on investment. So I should really be looking to move that money into longer-term investments. But I can take a while to get to the goal.