Amazing Coincidences

I recently did something that you’re not supposed to do. I bought a (new) house before selling my existing house. This made moving easier. I didn’t have to worry about “timing” the close, nor have to entertain real estate agents/buyers until after having left the previous place.

But financially, it made things a challenge. In order to swing it, I ended up selling a lot of my investments in 2021 to go to cash. I could then buy the new house, sell the old one in 2022, and presumably be back to reinvesting the cash with very little impact to my finances overall.

Boy, was I naive! And a little lucky.

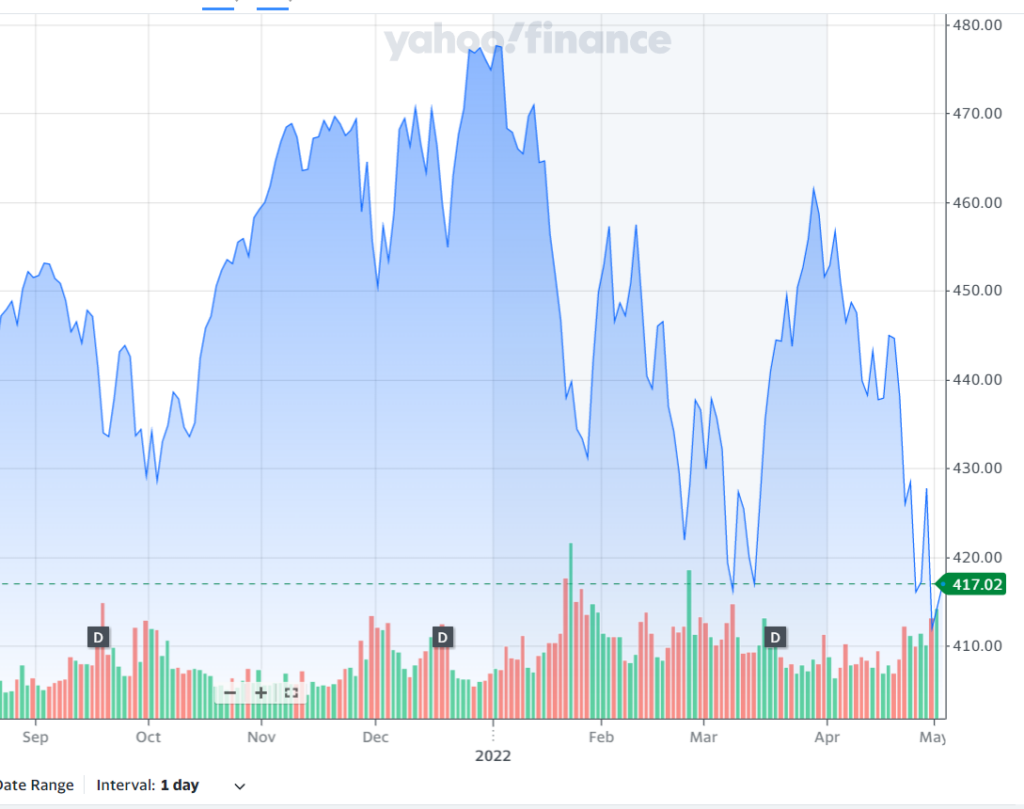

I started to sell my portfolio at the end of 2021 to get into cash. A little in October, a bit more in November, and most in December. By mid-December, I was pretty much all cash and out of the stock market.

Coincidentally, I had a BIG check to write to the government for taxes in December as well. So it was a double-whammy. Buying a house, and paying taxes in the same month.

Am I lucky? Because the market is down roughly 15% so far this year. Technology is down more.

In February, I sold my house in Toronto. It appears I sold my place exactly one week before the top of the market. It would certainly sell for a lot less if I listed it today.

So that’s a triple-whammy I guess. Forced to sell stocks pretty close to the recent highs for tax reasons and to buy a house. And decided to sell my house pretty close to the recent highs for real estate where I live.

It’s taken a while for me to catch up financially to where I was. The old house “closed” at the beginning of April, and my checking account is full. I now have to decide where to deploy the funds.

I can’t even be excited about jumping back into the stock market. The Internet is full of bad news. Inflation is at record highs. Government raising interest rates at an accelerated pace. War! Predictions of a recession.

I rarely do this, but for now, my money is sitting in a bank “Certificate of Deposit” (CD) – or we call it GIC in Canada. Earning an amazing 1.6% per year. Which is better than 0%, but well behind the 5.5% official inflation number.

Yesterday, I put a baby toe back into the market. I’m going to try to document that process on this site. It’s still to be determined how much I share about the details for privacy reasons. But we’ll see.