The Bear Case for Canadian Stocks in 2025

It’s impossible to predict the future, especially the stock market. Even when the economy is bad, the stock market can do well. And it can certainly over-react to news at any time. And recover faster than anyone expected. So this is all speculation and there’s no way to predict the future.

But let’s examine one possible Bear Case for Stocks. Particularly stocks in Canada but this could apply worldwide.

1. Past History Can Predict Future Results

Looking at a chart of the US S&P 500 performance in 2024, it looks like a straight line up and to the right, with only a few weeks of pullbacks in between.

S&P 500 in 2024

The S&P 500 has returned 25% in 2024. And that’s after a bit of a pullback in the last couple of weeks.

Since Jan 1, 2009

Since January 1, 2009, the S&P 500 is up 566%. There are some bumps on that line, but again, it’s basically a straight line up and to the right, as long as you can be patient during the drawdowns.

I also overlaid the Canadian TSX Composite index. It’s up 176% since January 1, 2009.

$10,000 invested into Canada in 2009 would be $27,645 today. While the same $10,000 invested in the S&P 500 would be $66,633.

There is a ridiculous difference in performance between the US and Canada.

Does this mean that Canada will begin to dominate the next 15 years after trailing the last 15? NO! Canada will continue to lag behind unless something changes. America continues to get more competitive with taxes, their trade policy, military policy and such. Canada focuses on sending $250 checks to people sometime next year.

Investing in Canadian stocks seems like a losing game in the long-term.

2. The Canadian Dollar Will Continue to Fall

The Canadian Dollar can be purchased for $0.6955 US at the current time. And experts predict that will continue to go lower.

The “loonie” has been falling steadily since mid-2021, when it was above $0.83. I don’t think anyone can imagine a reason for it to stop falling, given how things are going. Canadian interest rates are a lot lower, and Canada is not attracting business investment.

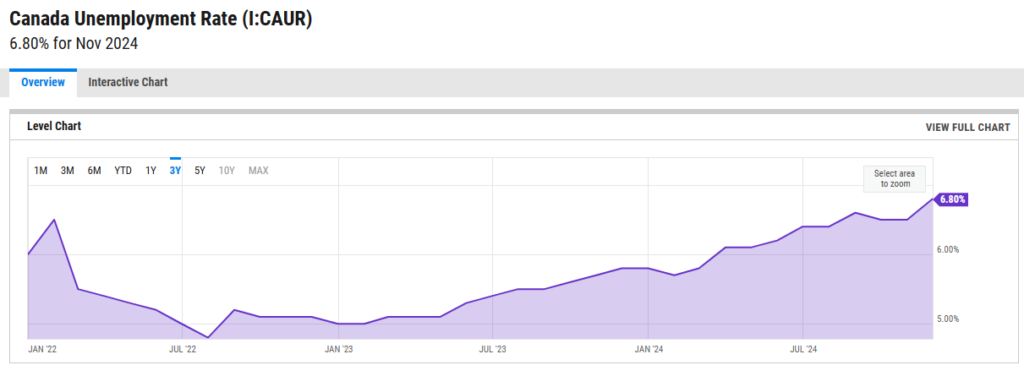

3. Unemployment Rate is Increasing

When people aren’t working, they aren’t doing a number of things. They’re not paying taxes, they’re not going to restaurants and spending on discretionary things, and they’re not paying their mortgages. A lot of bad things can happen when a larger number of a population is not working.

Not to mention, the increased government expenditure for benefits.

In Canada, the unemployment rate is creeping up and nobody is talking about it.

6.80% unemployment is actually quite high. It’s not hard to imagine 7% or 8% in 2025! This is the main economic signal that I am watching.

4. The Government is Fragile and In No Position to React to Economic Changes

The Canadian Finance Minister quit last week, in part, because the Prime Minister prefers to use “gimmicks” (her words) to stay in power instead of actual sound economic policies preparing for winter. His own party is asking him to quit, and so far he’s resisting. There appears to be no mechanism to remove the government from power quickly.

Many times over the past couple of years, the government has tried to buy their way out of crisis with borrowed money. There is supposedly a $250 cheque coming to working Canadians in the Spring for some unknown purpose. We’re currently at the start of a 2-month tax holiday on snacks (like potato chips) – because there is no tax already on healthy food. A couple of years ago, they sent out $500 (one-time) to renters to help with rent. And on, and on, and on…

All this to say, it looks like the Canadian government is certain to fall in early 2025. The current leader is trying to hang on to power (and technically he can stay in power until the Fall of 2025). But it doesn’t look good right now.

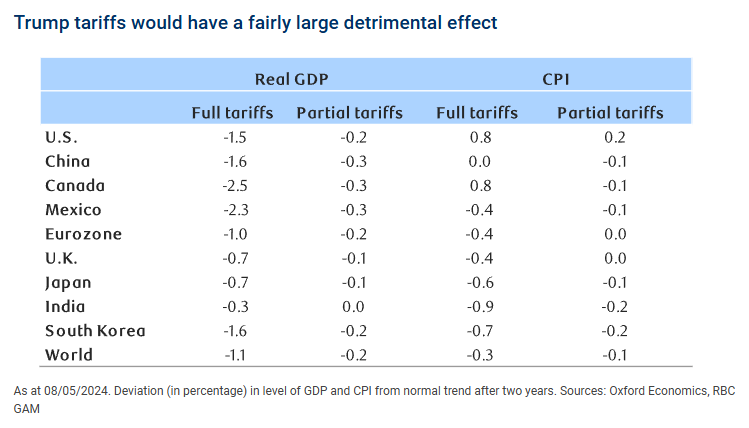

5. There’s a Looming Economic Threat that Seems Impossible to Avoid

In actual fact, the Canadian economy is under threat from the United States and there doesn’t appear to be any way to stop it.

Trump has said there will be a 25% tariff on ALL Canadian imports.

There will likely be a trade war with the US in the Spring.

It‘s possible that only some items become subject to tariffs. We’re still talking about a hit to Canada’s GDP.

And if Canada is somehow able to avoid tariffs, they’d have to make certain concessions to the US in order for that to happen. More harm to Canadian business. An increase in imports and a reduction of exports is the goal. That’s not good, long term.

6. The Coming Economic Recession

All of this adds up to a lot of “headwinds” as they like to say on CNBC.

7. How Do I Act?

I’ve said a few times before, I am not a trader. But I’m also not stupid. I should probably not be holding on to a lot of Canadian dollar denominated assets or Canadian companies in 2025.

As a result, I think it’s time to trim back on my Canadian holdings. I probably should sell 50% of what I own in the following.

- Hamilton Enhanced Multi-Sector Covered Call ETF (HDIV.TO) – sell 50%

- BMO Money Market Fund ETF Series (ZMMK.TO) – sell 100%

- Global X Gold Yield ETF (HGY.TO) – sell 100%

I will have to crystalize a capital gain when I do so, and owe taxes in 2025. I don’t think there’s a way for me to avoid this. Waiting until January won’t reduce the tax or when it’s paid (in my circumstance).

To offset the capital gains, I sold my Russell 2000 which is down 8% from where I bought it just a couple of weeks ago. This should result in almost no taxes.

8. Where to Put the Money?

Where to go for a safe, secure 10%? Lol

There are a couple of ETFs that deal in US Government Treasuries, right.

- Global X SPAY – Short-Term U.S. Treasury Premium Yield ETF – paying 7.75%

- Global X MPAY – Short-Term U.S. Treasury Premium Yield ETF – paying 9.50%

- Global X LPAY – Long-Term U.S. Treasury Premium Yield ETF – paying 11.35%

These things invest in US government bonds, and then use options on those to generate income.

The other idea is to go into global stocks and emerging markets. Traditionally, these have underperformed the US market. But perhaps it serves to reduce risk.

- Global X EQCL – Enhanced All-Equity Asset Allocation Covered Call ETF – paying 11.01%

- Global X EMCL – Enhanced MSCI Emerging Markets Covered Call ETF – paying ~12%

- Global X EACL – Enhanced MSCI EAFE Covered Call ETF – paying ~11%

EAFE is an acronym for developed markets that excludes US and Canada.

The word Enhanced is a giveaway that the include 25% leverage so they get to juice the returns a bit that way. There are also un-enhanced versions.

Out of all of these, I’ll choose the MPAY ETF for good medium-term treasuries using a covered call strategy. And also EQCL which covers worldwide stocks using a leveraged covered call strategy.

This raises my rate of return (as these pay 9-11%) and diversifies away from Canada a bit more.

I made the trades today, on Christmas Eve.