Should I Consider Adding Blue Chips?

I watched a video today that made a compelling case for buying some big dividend-paying companies at current prices. The five names they listed were:

- Intel

- Altria

- T. Rowe Price

- 3M

- Walgreens

I am not sure what to think of those names. Let me investigate.

Intel (INTC)

In recent years, I’ve come to believe that companies like Intel have stopped innovating and are falling behind in chip manufacturing. They’ve struggled as other competitors have made smaller and smaller chip sizes. Intel produces a 10 nm chip while TSMC already produces a 5 nm chip. So I’ve not been a big fan of Intel as a company.

But they are a solid cash-generator.

Their stock trades at an impressive 6.7X PE ratio. That is, the company earns in profits the entire value of the company every 7 years. That’s really low for any stock, and really low for a tech stock.

They have impressive profit margins of 54% gross and 32% net. They pay a 3.6% dividend, which isn’t high. But the key item is that the company is really undervalued when it comes to its competitors. Thus, one can say that the stock appears severely undervalued.

So can the stock rise in the next 5-10 years to get closer to its fair value? Or will the fair value come down to meet the current stock price?

In the meantime, I’d be earning a 3.6% dividend to hold the shares. It’s an interesting idea.

Phillip Morris, I mean Altria Group (MO)

The tobacco industry seems to be an odd idea. I’ve never smoked and would never consider it. If the government were to ban smoking completely, I wouldn’t mind.

Altria Group is one of those companies that makes a lot of money. Their P/E is pretty high at 25.8x. Their gross margins are decent at 66%, but their net margins are low at 14%.

Altria’s P/E is higher than almost all of its peers. If I wanted to invest in tobacco, almost every other option would be cheaper.

They also have a lot of debt. There’s almost no shareholder equity. It’s the bondholders that own this company, not shareholders.

I won’t be investing in Phillip Morris after all.

T. Rowe Price (TROW)

I hear a lot about T. Rowe Price in the stock forums. Some people love this company. Not sure about investing in a mutual fund company at the start of a possible recession. But the numbers can be decent.

The P/E Ratio is good at 9.8x. This is considered a fair value by the markets. Their profit margins are good at 60% gross and 36% net. They have almost no debt. They pay a 3.9% dividend, and it should not be hard for them to continue that.

This seems like a well-run company. This should go on my list as a potential investment.

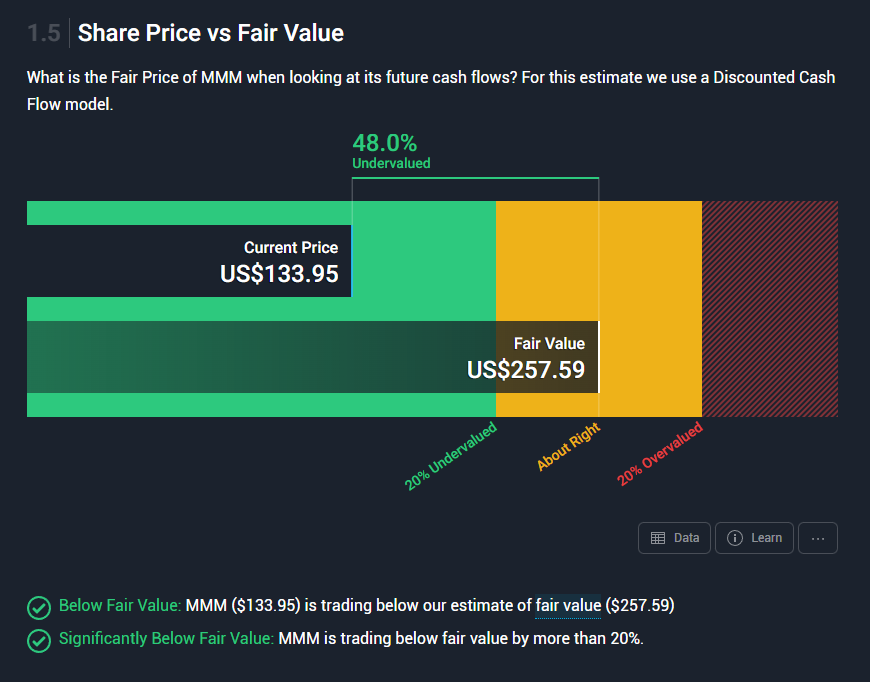

3M (MMM)

3M is a good old American industrial company. They make Post-It Notes. I am not sure they are poised for great growth in the future, but I bet their financials are stable and solid in good times and bad.

It has a P/E Ratio of 13.6x, which is not bad. Gross margins of 46% and net margins of 15%. For an industrial company, that’s not bad.

SimplyWall.St considers it massively undervalued based on future cash flows, at 48% below fair market.

Like Intel, this could be a boring manufacturer that isn’t in the news every day like Apple or Microsoft but will be worth way more in 5-10 years than it is today. It could be a bedrock company.

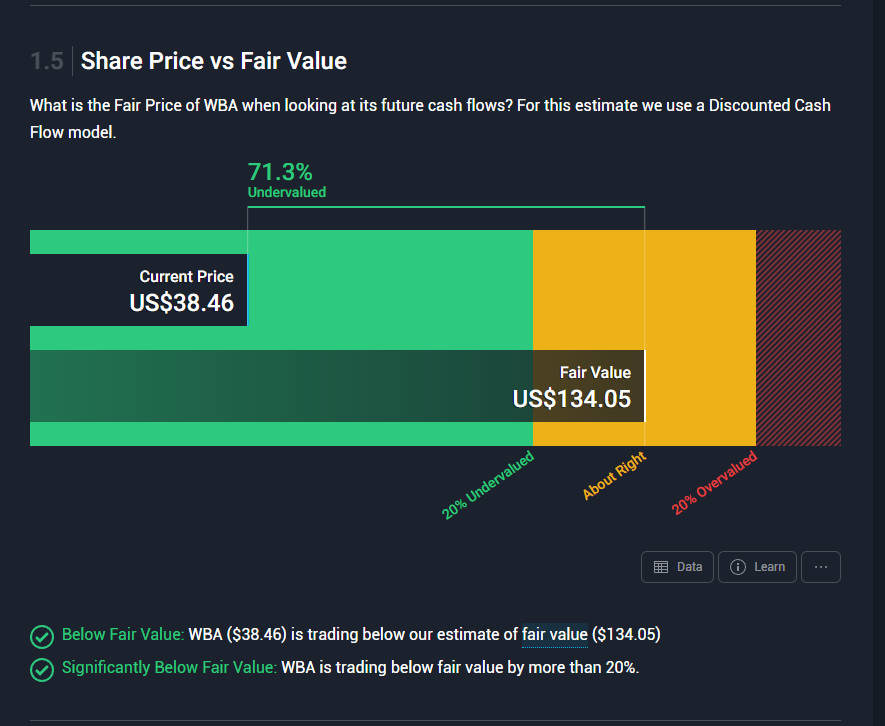

Walgreens Boots Alliance (WBA)

Drug stores seem like a recession-proof business. People will always need to run to the local drug store for over-the-counter meds, makeup, snacks, or Halloween costumes. Those things aren’t at risk of being disrupted by Amazon or Walmart.

Walgreens has a 6.5x PE ratio, which is OK for a retail store. Margins are not great in retail at 21% gross and 3.8% net. But that’s expected. It has a solid 5.0% dividend, which is well-covered by earnings.

SimplyWall.St considers this massively undervalued based on its free cash flow.

This could be a good pick.

Conclusion

There are a couple of good ideas on this list. I could invest in Intel, 3M, and Walgreens as solid companies that make large amounts of free cash flow and are potentially undervalued. I would benefit from a small dividend from each, while the stocks have the potential to go up by way more than that.