Goodbye $BABA Deep In The Money Options

Perhaps there’s a way to trade deep-in-the-money options profitably. I haven’t found a good strategy, and I picked the wrong stock to play with. BABA was a boat anchor, sinking, sinking, sinking.

The strategy I was trying to follow was hypothetically foolproof. Every month, I can sell a DITM call against 100 shares of a stock. “Theta” decays a few cents per day, reducing the price of the short option. Then, a month later, I can roll the call another 30 days forward. Monthly, I collect another dollar in premium (per share) and just wait for time to pass.

Theta in stock options measures the rate of decline in an option’s value as time passes, known as “time decay.” It indicates how much value an option loses each day, with decay accelerating as the expiration date nears. This metric is vital for option traders, as it affects the timing of buying or selling options. For option holders, theta represents a risk of diminishing value, while for option writers, a high theta can be beneficial as the sold option loses value over time.

My main challenge, of course, is ensuring that my stock doesn’t get called away while I’m in an unprofitable position. This means the stock should be relatively stable (or increasing) and not falling.

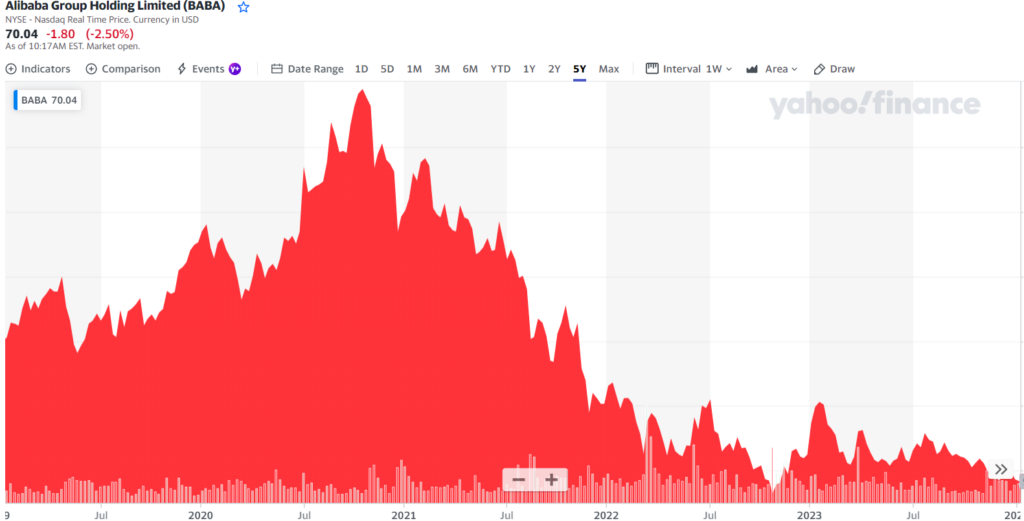

$BABA was not a good pick for that. It’s been falling.

The story so far:

- Sep 25: Bought 100 shares of $BABA, at $86.72 per share

- Sep 25: Sold to open 1 NOV17 $70 call at $17.75

- Adjusted cost base: $68.97

Then, a month later:

- Oct 26: Buy to close 1 NOV17 $70 call at $13.27

- Oct 26: Sold to open 1 JAN19 $70 at $15.09

- Adjusted cost base: $67.15

Then, a month later:

- Nov 27: Buy to close 1 JAN19 $70 call at $8.24

- Nov 27: Sold to open 1 FEB16 $70 at $9.16

- Adjusted cost base: $66.23

Then, in January:

- Jan 16: Buy to close 1 FEB16 $70 call at $3.03

- Nov 27: Sold to open 1 MAR15 $70 at $4.52

- Adjusted cost base: $64.74

As a whole, the trade is profitable. Barely.

The option would cost $4.65 to buy back, and BABA is currently trading for $70.07. So I’m in the profit around $0.70. Not including trading fees.

The whole trade is currently about “45 Delta”. For every $1 that the stock was to move, I would gain or lose about $0.45. So, if BABA were to rise from $70 to $80, there would probably be another $4.50 in profit.

Delta in stock options represents the rate at which the price of the option changes relative to a $1 change in the underlying stock’s price. It’s a measure of the option’s price sensitivity to the stock’s movement, varying between 0 and 1 for call options, and 0 and -1 for put options. A high delta suggests the option price will move significantly with the stock price, making it a key factor for traders to consider when predicting the option’s potential change in value due to stock price movements. Delta not only aids in assessing risk and potential reward but also plays a crucial role in options trading strategies.

This is all pretty complicated. In fact, I think I’m tired of the BABA trade and might just get out of it, for breakeven.

So Much for 95 Delta

When I first put this trade on in late September, the NOV $70 CALL was 0.95 delta. That meant the stock market was assigning only a 5% chance that BABA would fall to $70 by November 17th. It’s trading at $70.07 today as I write this on January 15… Geez.

Right now, the February 16 $70 call that I have sold has a 0.65 delta. I am in the money, but no longer deep in the money. I might have to trade down $5 or $10 to get back deeper into the money.

So what’s my plan?

I decided to get out of the BABA trade entirely. It’s not worth the time following this constantly falling stock, and trying to scalp the options premium is an exercise in futility.

The trade went from “deep in the money” to “at the money”, and that’s just not what I was trying to do here. I could have lowered the strike prices some more, but what for?