New Goals for The Rest of 2023

In the last post, I reviewed my goals from a year ago when starting this website.

2022 Goals

- Goal #1: Being Fully and Efficiently Invested

- Goal #2: To Make From Investments What I Make From My Business

- Goal #3: Rate of Return Across My Portfolio

How Did 2022 Go?

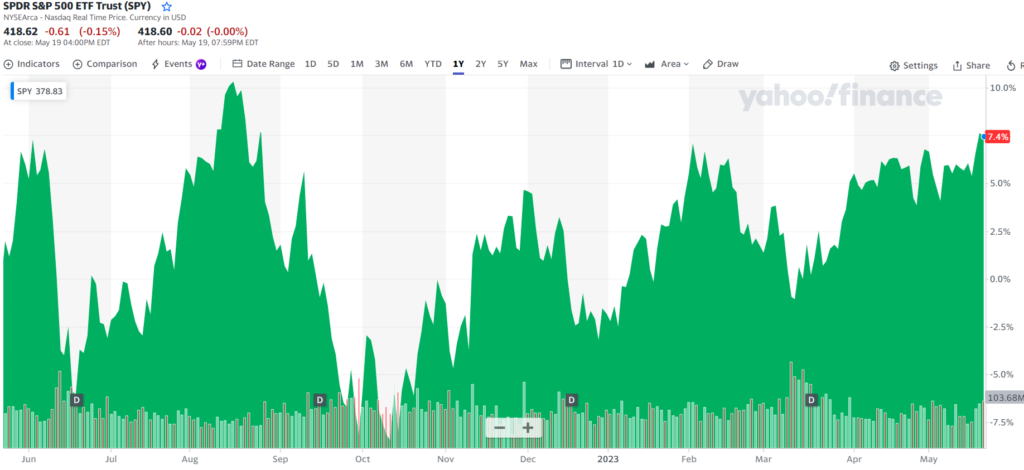

The stock market is (has been) quite a roller coaster ride. In one year, it has fluctuated from -8% to +10%. The graph below has five distinct “highs” and four distinct “lows” in one year.

How can it go from 6% down in June 2022 to 10% up in August 2022, followed by 10% down in October 2022? That’s 16% up in only two months and 18% down in the following two months!

That’s crazy.

It’s tricky to begin investing in a period such as this. (While I’ve been investing in stocks for 20 years, I started from an all-cash position last year.) So none of my investments have significant unrealized capital gains, making it easier to ride the waves.

Goals Changed

So my goal at the end of 2022 was changed part way through the year to become capital preservation with money market funds and short-term bond funds.

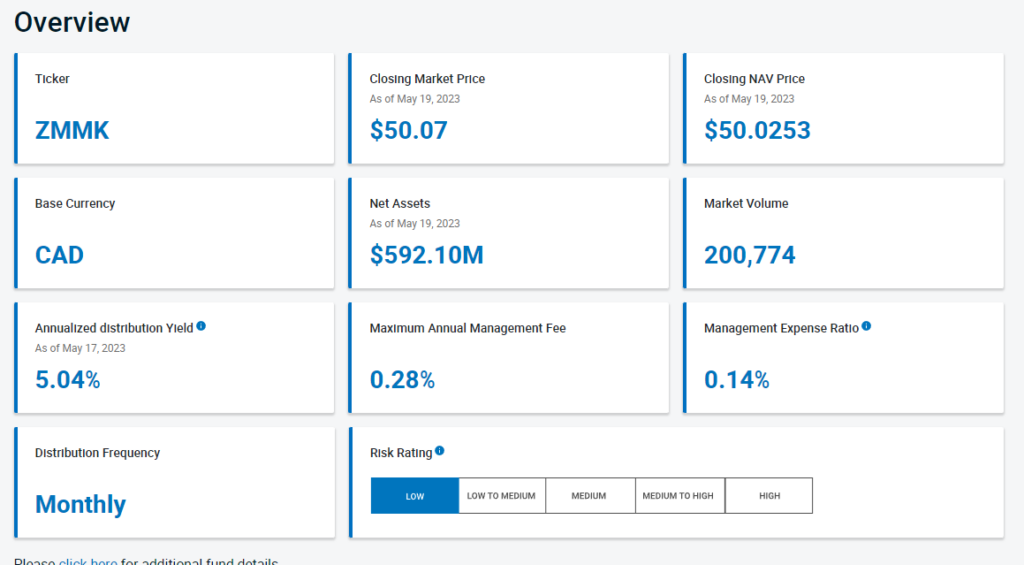

I’ll take the safe/secure 5.04% instead of hanging on to a +18%/-18% ride that nets 6% at the end of the year.

I invested 26% of my invested funds into ZMMK – BMO Money Market Fund ETF Series. That’s a lot, but it’s currently paying me 5.04% in distributions. Roughly 0.4% per month. It’s a low-fee fund.

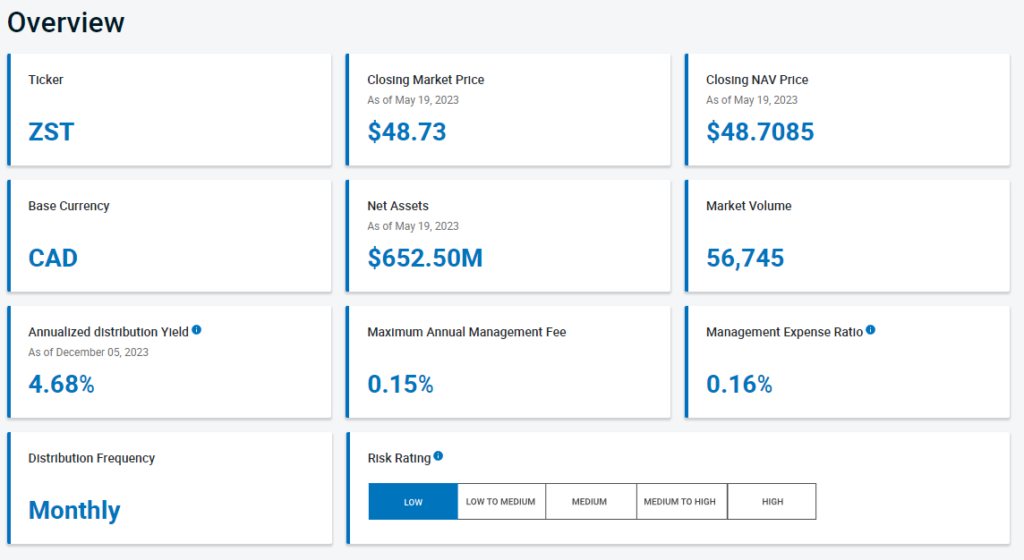

I also invested in ZST – BMO Ultra Short-Term Bond ETF. This fund holds 13% of my invested funds. This fund has Canadian government and corporate bonds. The good thing about Canadian bonds is that the government doesn’t fight itself over whether to repay them. It just does. It’s paying 4.68% distributions, also around 0.4%. It’s also a low-fee fund.

2023 Goals

So back to my goals for 2023. The following are my new goals.

- Goal #1: Being Fully and Efficiently Invested

- Goal #2: To Make Relatively Low-Risk Consistent Returns

- Goal #3: To Keep Pace with Inflation

Again, this is slightly different from my goals from a year ago. Reducing the risk for more stability of income.

Goal #1

I still want to be fully invested in something that has a return. The amount of cash I have in my checking accounts is a high source of frustration. It’s hard to explain why this still is a problem one year later. It is difficult for me to have almost no cash in my bank account “in case of emergency,” even if that cash is conveniently invested in money market funds with no risk.

Goal #2

I decided not to try to match my business income with investment income. Since I make a good income from my business, I don’t require income from investments to survive anytime soon. The idea of replicating my entire income from investments was inspiring but unnecessary. I only need enough money to live; my investments already return that.

Goal #3

Sitting with a lot of cash is such a waste. It’s like intentionally losing 6% per year. The bank pays next to nothing in interest. One of my top financial mistakes HAS to be having so much uninvested money. That has to stop.

Current Portfolio Breakdown

My current investment breakdown is:

- Being 39.5% invested in money market/short-term bonds is a bit high, but I don’t mind. While the funds are paying 4-5%, that’s a decent rate of return. And is close to the rate of inflation.

- Another 45.5% is invested in the broad market. S&P 500, banks, utilities, and such. I will benefit from the long-term rise of the stock market and not be hurt too much by the fluctuations.

- Another 6% is in high-yield bond funds.

- And 8% in individual stocks.

This doesn’t include the 37% I have just in cash. (Part of that is a GIC that is expiring in the next 30 days!) I hope to return to investing that into the market this month now that I’ve paid the various governments their fair share in taxes for the year.

These are my goals for 2023. I will start to track them and think more about how I can achieve them.