Still Waiting for Bonds to Return

There are 100 different examples of “financial things breaking” this year, but one that isn’t often discussed is how the bond market and the stock market rarely (if ever) crash simultaneously.

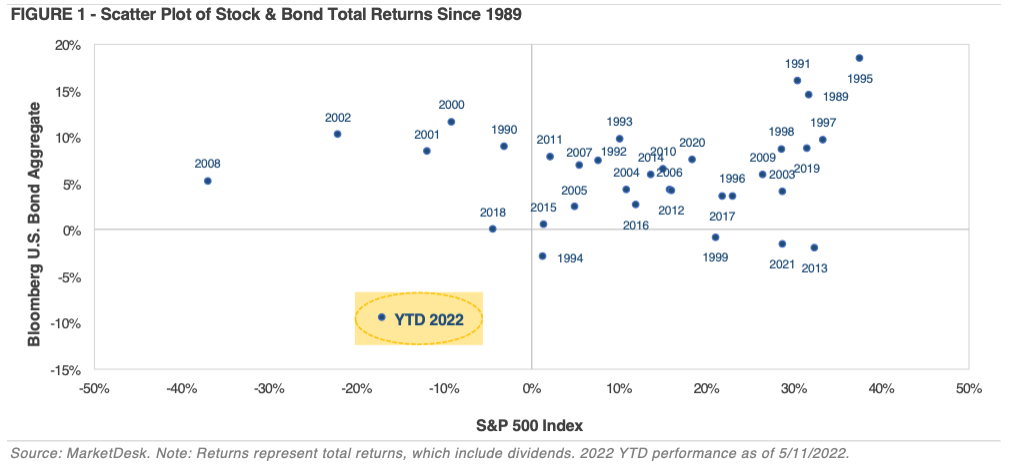

The S&P 500 is down nearly 24% year-to-date, and the Bloomberg U.S. Aggregate Bond Index has surrendered about 16%. Should both indexes finish the year in the red, it would be the first time that has happened in decades.

CNBC

In the chart above, we can see that there are years when both bonds and stocks have a positive return, some years where stocks have positive returns and bonds have a negative return, and some years where stocks have a negative return and bonds have a positive return. But 2022 might be the first year since 1969 when both stocks and bonds both had negative returns.

Normally, bonds are a hedge for stocks. As the stock market rips, bond performance is muted. And then, when stocks fall, bonds get their time to shine. But in 2022, both are having horrific years. That’s not supposed to happen.

I guess what is causing this is the around 8-10% inflation that many advanced economies are going through. Inflation causes interest rates to rise rapidly, which causes bond prices to fall. I’ve also read that the rise from near 0% interest rates to now almost 4% has never happened before so quickly – in just over six months.

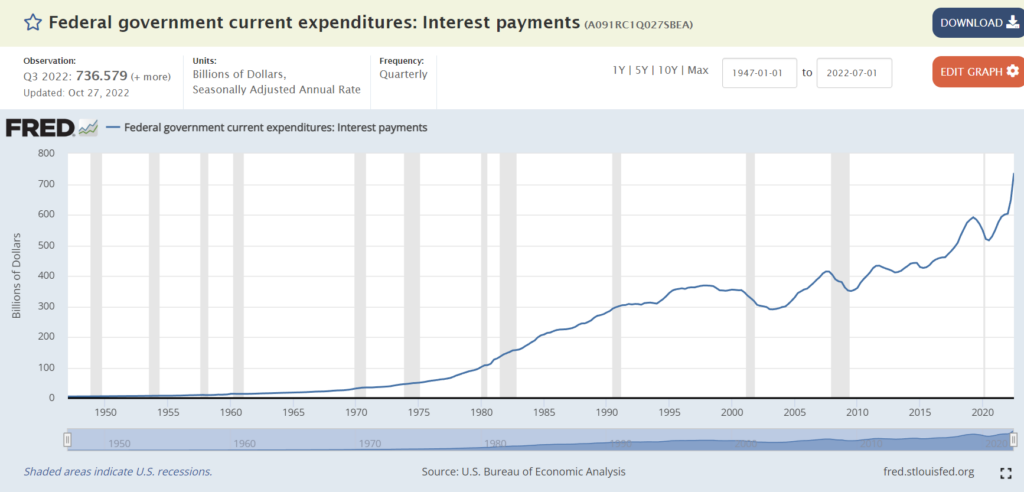

I believe that we are almost near the end of the interest rate increases. It’s hard to imagine interest rates going to 5% in this day and age of the record-high debt. The annual interest payments on the US debt now exceed the amount of money they spend on their military. Since they are running high annual deficits, this amount will only increase yearly as the US goes deeper into debt.

$746 Billion per year in interest payments, currently. Wow. $2,000 per American citizen per year.

(The total Federal debt is almost $94,000 per citizen (including babies) or $248,000 per taxpayer. How are they ever going to pay that back? Another story for another day.)

Today I added some money to the markets. Just adding to existing positions and lowering my cost basis.

I bought some more bond funds.

I added to Invesco Senior Income Trust (VVR) because I still like the stock, and I haven’t lost any money in it since I bought it. It trades at a discount to NAV as well. It returns a nice 10.4%.

I added to PIMCO High Income Fund (PHK) because I could lower my cost basis a bit. It returns a nice 11.95%.

I also added to DoubleLine Income Solutions Fund (DSL). It’s good to lower my cost basis as this fund has fallen quite a bit from where I bought it. Still, it now returns 12.23% to investors.

I decided to dollar-cost average down on RiverNorth/DoubleLine Strategic Opportunity Fund (OPP). This fund has fallen a lot and currently trades at a historically-high discount. It pays 20%! This is crazy. Maybe they have to cut their distribution at some point, but buying this at a 10%+ discount seems like an opportunity. I should buy more.

Or maybe I shouldn’t be too greedy. But I might regret not getting more at the 20% yield. OK, I convinced myself to double this position…

These investments reduce my cash pile by 2-3%.

Slowly, slowly… making my way towards my goals.