Dipping My Toe in Closed-End Funds

I’m a bit impulsive sometimes.

I am reading a book that talks about closed-end funds (CEFs) for income (“How to Retire on Dividends: Earns a Safe 8%, Leave Your Principal Intact“) and the idea makes sense to me. I started digging into the details even more, and I found a few that look appealing.

What is a closed-end fund (CEF)?

Investors give a closed-end fund a pile of money at the inception of the fund’s life – for example, $300 million – and that’s it. That’s all the money that it has to invest. The fund manager can then go to the market and invest his/her strategy without worrying about redemptions.

The shares of the fund trade on the stock market. Quite often, the true market value of the investments made by the fund (net-asset value or NAV) can be different than the share price.

Let me say that again, louder.

The Net Asset Value is usually different than the share price.

Some funds are popular and always trade at a premium to the NAV. These funds are run by famous managers, have good advertising or sales teams, or provide access to investments that are not available to the general public. Investors are betting that the value of the investment will still rise to overcome the premium, or that the premium will still be there when they are interested in selling.

Some funds trade at a discount to the NAV. Imagine being able to buy $100 worth of assets for $90. This is available in the closed-end fund market for some reason. And the “$100 of assets” refers to the true current value in some cases. For instance, a closed-end fund can own Apple, Google, and Amazon, and be trading at 90% of the value of its holdings.

The B-Word

The closed-end funds I am looking at today deal mainly in fixed income, otherwise known as bonds.

You may be shocked by this. I have long held the belief that bonds are toxic in a rising interest rate environment. Well, we have already seen wide destruction in the bond space in 2021 and 2022. “Everybody knows” that interest rates are rising this year. In fact, the market has a prediction about what the interest rate will be at the end of the year. This is priced in.

In my last post, I showed a chart about one such “income fund” that has declined 28.1% in the past 12 months. Bond funds have been decimated. A 28.1% drop for one bond fund exceeds the amount that the S&P 500 has fallen in the same time period – 11.6%.

The Return of Bonds

Well, interest rates are back up. The US 2-year treasury bond was offering a 0.10% yield about a year ago. And today, it’s above 3%.

The US Federal Reserve is raising their “Fed Funds Rate”, slowly too. And it’s expected that it will get to 3% this year too.

Now 3% is not a great interest rate to earn, but it’s many times better than 0.1%. Approximately 30 times better, in fact. 🙂

So now people are starting to wonder when bonds begin to be an attractive investment for investors seeking income. In fact, maybe it’s time.

I’ve watched a number of interviews with fund managers, and read a few articles too, thinking that the time to enter bonds might be coming.

I’m not saying “go all-in!” But bonds might have a place in my portfolio for income over the next 20 years…

One video I recommend is from “Bond King” Jeffery Gundlach of DoubleLine. I guess he does these monthly updates. I’ll be watching every month I guess. Packed with great charts and information.

Certainly with the bond funds down 50% or more in the past 12 months, a lot of the risk has been taken off the table. Maybe there is some room for the funds to fall some more, but how much lower can it realistically go?

The Income!

I haven’t even mentioned the income part yet.

So you can buy a closed-end bond fund, at a slight discount on its NAV. 5-10% discount seems common.

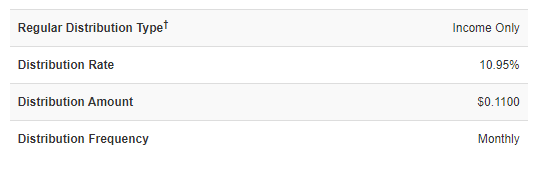

Plus some of these funds are paying a crazy distribution rate currently. Here is one closed-end fund offering a 10.95% distribution on invested funds.

Now, “what’s the catch,” should be your first question. You’re right, there is a catch.

Beware of Return of Capital (ROC)

The first thing you need to look at is, where is this income coming from? How can a sleepy bond fund pay 10.95% back to investors?

Return of Capital is one way. Return of Capital is best described as giving you your own money back.

Let’s say, you gave me $100 to invest, and I promised you $1 per month in return. You quickly calculate that as $12 per year or 12%. You’re excited by that. And so my challenge (as the fund manager) is to invest $100 and make 1% per month. Oh but wait. I need to make a profit too for all this hard work so I charge 2% per year as my fee. So I need to make 1.16% per month to cover your profit and my fee.

In the first month, I invest in $META. The stock only goes up 0.5% in that month. Your $100 became $100.50 after 30 days. That’s less than what I need to send you the $1. So what I do is sell $1.16 worth of $META stock. I send you the $1, pocket $0.16 as my fee, and your $META is only worth $99.34 now. ($100.50 – $1 – $0.16)

I sent you $1 but the fund only made $0.50 cents profit. This is partly a return of capital. $0.50 of what I sent you was profits, and $0.50 of what I sent you was capital. The value of the fund dropped as a result, but your cost basis (ACB) also dropped by $0.50.

If we do this every month for a year (assuming $META goes up by 0.5% per month), you’ll have received your $12 in profits, and I will have received my 2% in fees. BUT the fund will only be worth $91.84 after 12 months. $8 of your $12 in profits will effectively be “your own money back” or be lost to fees.

So I have to avoid funds that always need to return of capital. Maybe it’s ok to do it once or twice a year, but if 50% of your distribution is the return of capital, the distribution is an illusion.

Leverage

A lot of these funds use leverage. Some leverage is not a bad thing, but it does add to the volatility of the NAV.

One of the reasons these funds can return a higher distribution than I can get myself is that they are borrowing money to buy more of the asset. I have seen 30%-40% leverage as being quite common. So the fund might normally only return 8%, but with leverage, it returns 12%.

Junk Bonds and Mortgage-Backed Securities

One of my favorite movies is “The Big Short“. I have watched it three or four times. Maybe more.

When I look at the holdings of some of these closed-end funds, I have a mini-heart attack.

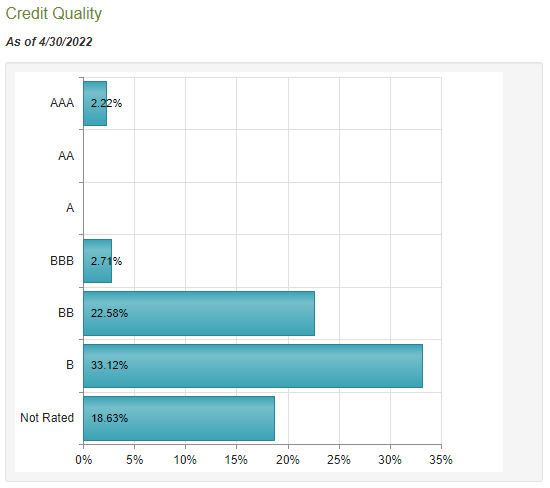

BBB or better is considered investment grade. Pensions and grandmas invest in investment-grade bonds.

Most of the bonds in this fund are BB and B. And some have no rating. I need to really think hard before investing in things that invest in those.

Now here’s Margot Robbie in a bubble bath to explain mortgage-backed securities.

I’ve heard a lot of people say, we’re not in a subprime crisis like we were in 2008. People don’t have these “adjustable-rate” teaser loans, and “no income, no job” loans have also gone away. Banks aren’t giving out loans at 100% loan-to-value. So we’re not looking at the same “risk of default” that we were in 2008.

I have to trust that to be true. Because these closed-end funds suffered greatly in 2009. The same funds that I am looking to buy today crashed mightily back then.

Dilution Through Secondary Offerings

Remember that I said at the beginning of this post that closed-end funds differ from mutual funds and ETFs in that they are closed. They cannot accept new money and they don’t have to sell assets to redeem units. That’s why the NAV and the share price are different.

Well, closed-end funds have ways of raising fresh capital. They can go to the market with an offering to sell more shares, just like any other company can.

Some closed-end funds do this a lot. Particularly if their distribution is higher than their income.

For instance, in my fictional example above, where I took your $100 to buy $META, and paid you $1 per month as a distribution. Half was from the capital gains of META and half was giving you your own money back. What if the price of $META went down, not up? So if META was losing 1% per month and I still have to pay you $1 per month. In that case, the entire money you are making is the return of capital, and at the end of the year, your fund might only be worth $75.

You earned $12 in income and lost $25 in capital.

The fund will run out of money in a couple of years at this pace. So what I can do is ask you if you want to invest another $100. You’re happy, because you’re earning 12% return on your money. It’s a decent offer. But to sweeten the deal, I offer you shares at a further discount to the current NAV. What if I gave you $110 in shares in exchange for your $100? That’s even a better deal! A further discount! So you might be tempted to give me another $100. Or you might beg me to accept $500 from you.

This dilutes the existing shareholders a bit. If you decline to give me the $100, and someone else does instead, they’ll own $110 of the $175 in shares, and you’ll only own $65 of the shares. You lose $10 instantly by not being part of the secondary offer. So I want to avoid funds that do a lot of secondary offerings.

Distribution Rates Adjust

Some of the funds I’ve seen have an annual adjustment of the distribution. For instance, they aim to return 12.5% of the fund’s NAV per year. If the NAV falls after I purchase it, then it’s possible my expected monthly distribution will readjust to a lower value.

In my example above, if you buy $100 of my fund and expect $1 per month in year 1, if the NAV falls in year 2, you’ll receive less than $1. Let’s say it falls to $0.90 per month. Which is still good, but you were expecting $1. And your “in advance” calculations don’t pan out.

Risk

There’s some risk here. It’s not risk-free.

But I’m willing to dip my toe in the water. In the interest of learning, of course.

Today I invested about 1% of my portfolio in a set of three closed-end funds:

- Invesco Senior Income – VVR – 8.8% discount to NAV, 8.13% distribution

- PIMCO Dynamic Income Fund – PDI – 3.4% premium to NAV, 12.83% distribution

- PIMCO High Income – PHK – 6.0% premium to NAV, 11.29% distribution

I spent hours reading the details of each fund and understanding the dynamics at play.

I’ve checked the ratings of the funds on Morningstar. I’ve watched videos of fund managers and reflected on their current worldview.

I’m going to sit on that for a few months and watch the market play out a bit. When I see things are clearly turning around, I’ll buy some more.

Income For Life?

I can see myself holding these bonds for a while. (Maybe I shouldn’t speak too soon.) But if they really are paying out 8%-12%, without returning my own capital, then this is a good step toward my goal of an 8% annual return. If I can buy them cheaply while bonds are still unpopular, I can get in at a good price.